FXOpen Trader

Active Member

Strong Dollar Breaks the Reflation Theme – All Eyes on the U.S. Yields

2020 proved to be a challenging year for currency traders looking to forecast how the U.S. dollar will react to the pandemic. The Federal Reserve of the United States (Fed) immediately lowered the fed funds rate to the lower boundary (i.e., close to zero) and vouched to leave it there for as long as necessary.

On top of that, the Fed restarted the quantitative easing program, buying bonds to lower the yields on the short and long end of the curve. Furthermore, it opened USD swap lines with other central banks in the advanced world to provide liquidity and advert the strong dollar theme.

It worked.

The dollar initially appreciated as the world looked for safety in the face of the pandemic, but then the Fed’s plan entered into effect. Slowly at first, more aggressively after, the dollar started to lose ground across the dashboard.

Everything appreciated in dollar terms – the euro, the Australian dollar, the British pound, equities, and commodities alike. The bearish trend on the dollar was so strong that all investment houses forecasted an even lower dollar in 2021.

They were right.

The so-called reflation trade, where U.S. equities advance, the dollar declines, and risk-on dominates, was the theme for most of the first quarter of the year. However, the dollar started to show some strength recently on the back of a faster economic recovery, impressive vaccination campaign, and a U.S. administration that delivers.

What’s Next for the U.S. Dollar?

As we head into the second quarter of the year, the dollar trades with a mixed tone. On the one hand, it gained against the euro since the year started.

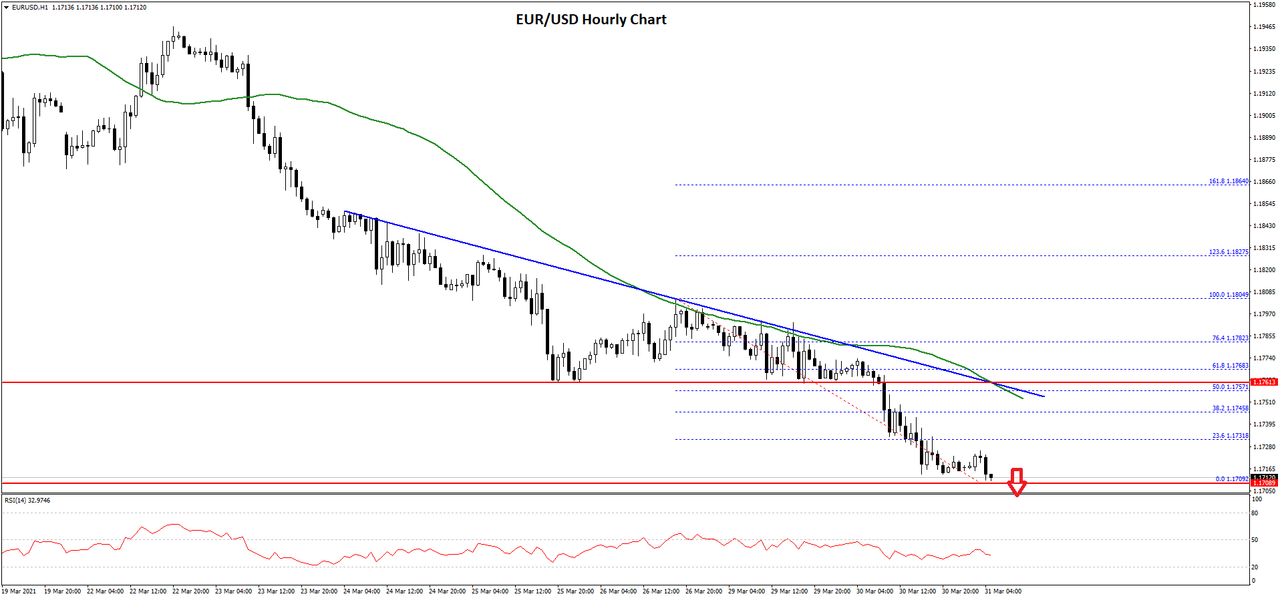

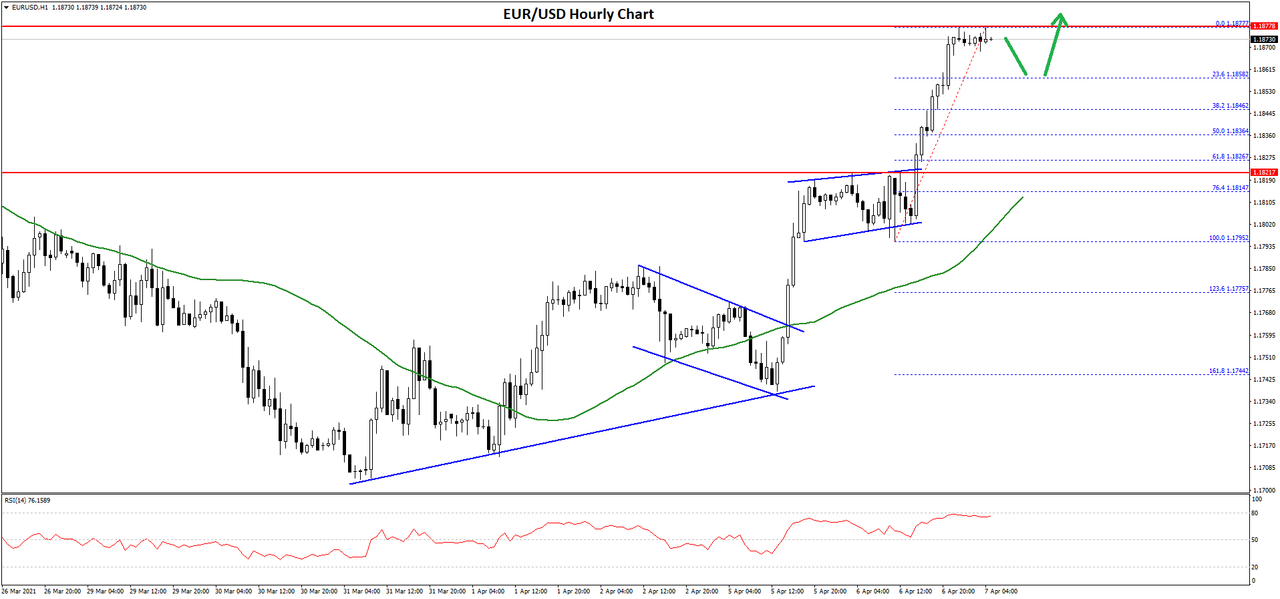

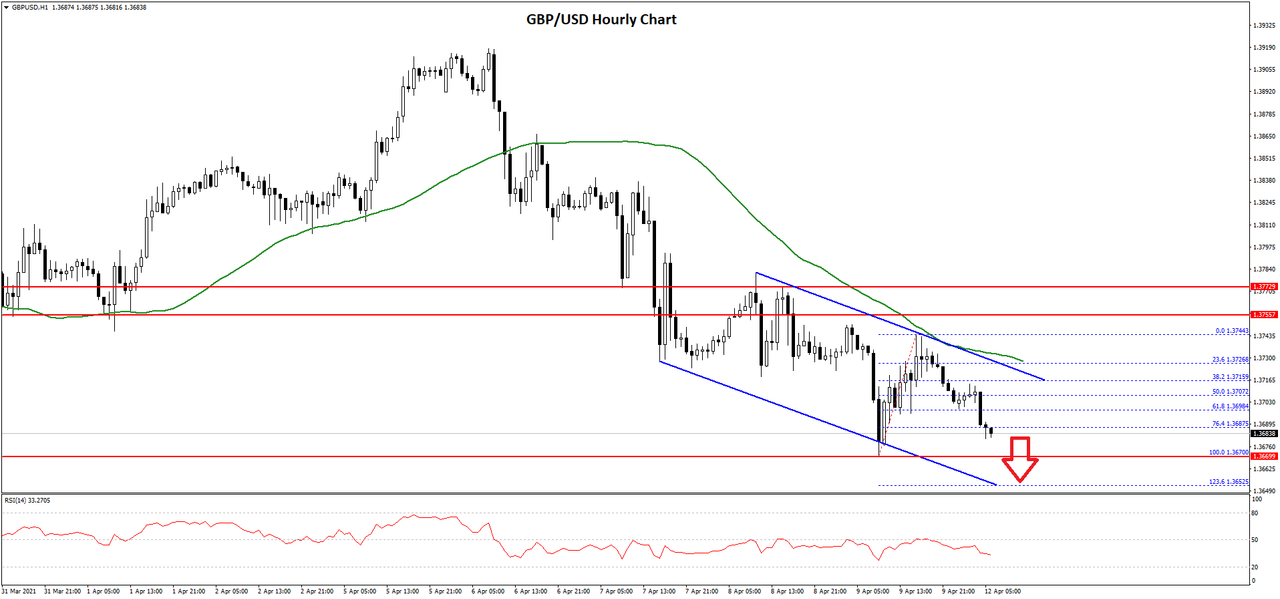

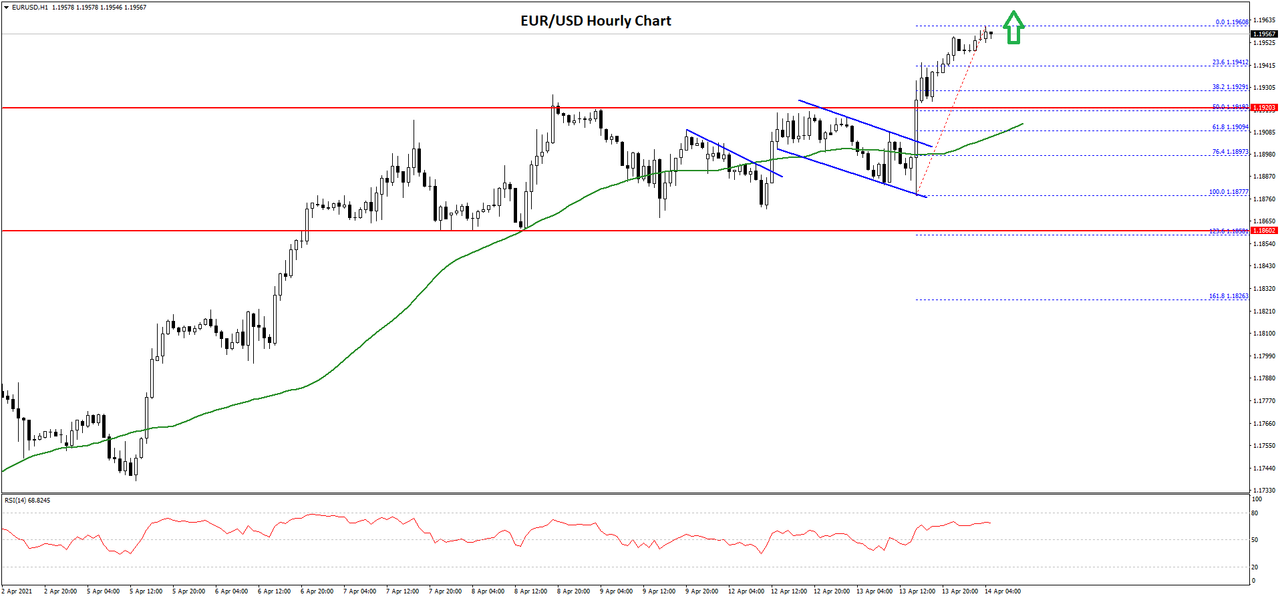

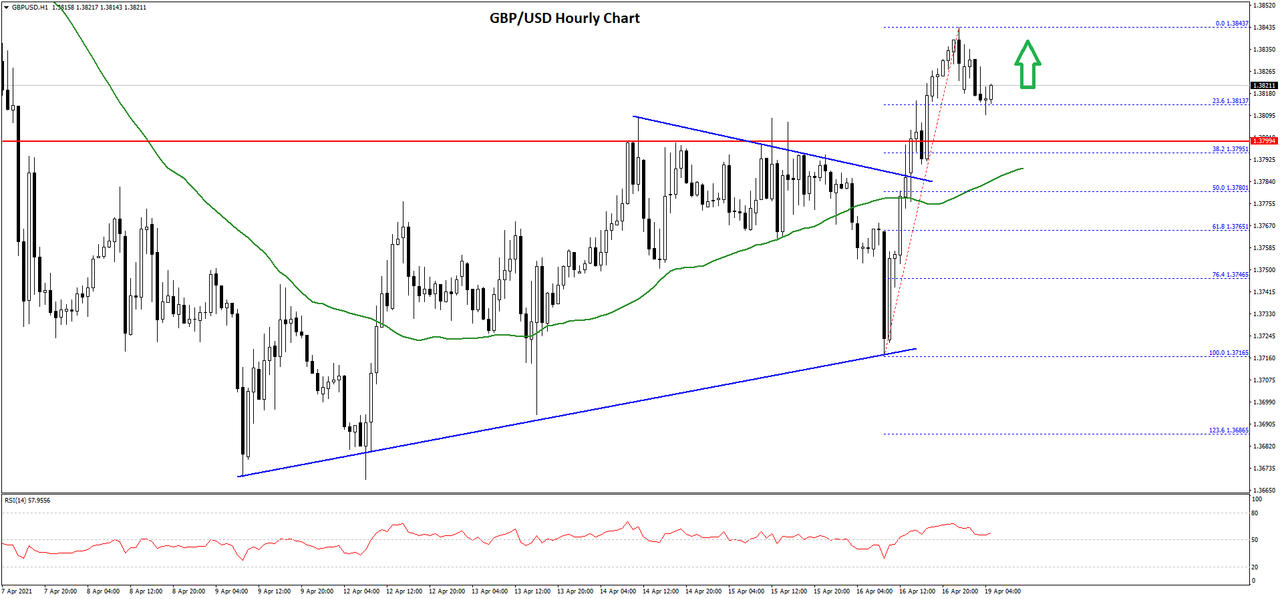

At the start of January, the EURUSD pair traded above 1.23, and last Friday closed below 1.18. Because the euro has the biggest weight in the dollar index, the move lower in the EURUSD exchange rate led to a reversal in the DXY.

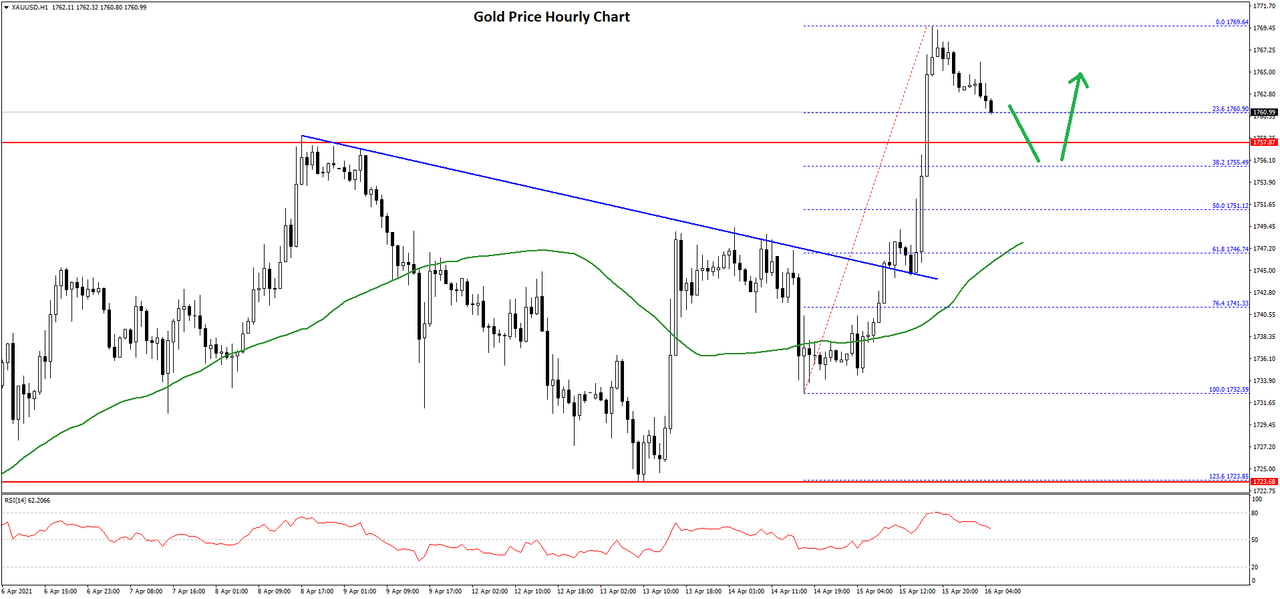

Gold made a new all-time high in 2020 – it traded above $2,000 last summer but is in retreat ever since. It is barely holding above $1,700 at the moment, and fears of higher inflation in the United States and the developed world are not enough to fuel a rally in the yellow metal.

The problem for the reflation trade and gold comes from the fixed-income market. The U.S. yields are rising, and whenever this happened in the past, gold weakened.

Put it simply, rising yields mean that investors flee the safety of bonds in search of higher returns in riskier assets. Effectively, it means that confidence is back and, thus, gold suffers as investors do not look for protection anymore.

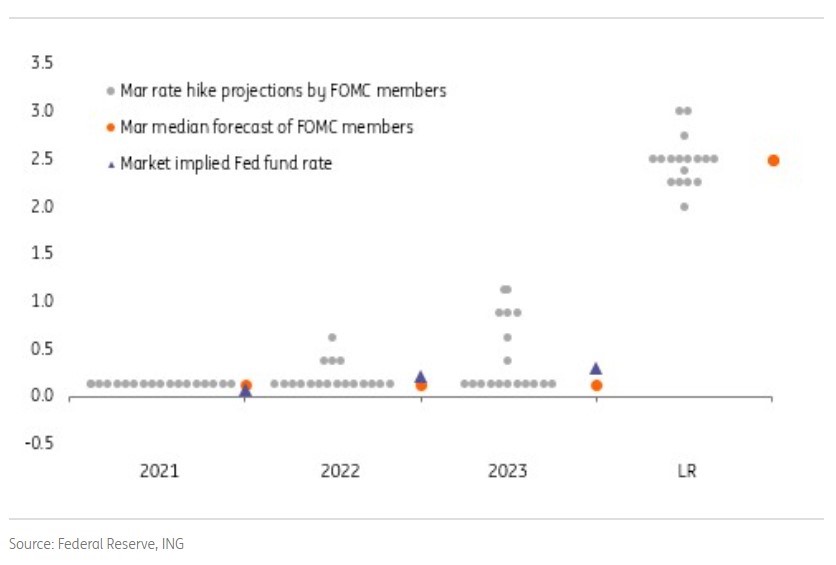

Higher yields also bode well for the dollar. Hence, before betting on a lower dollar, investors should first monitor the fixed-income market and interpret where the yields will go.

All in all, the second quarter will be extremely interesting. If the yields continue to rise, the dollar will have a hard time weakening.

FXOpen Blog

2020 proved to be a challenging year for currency traders looking to forecast how the U.S. dollar will react to the pandemic. The Federal Reserve of the United States (Fed) immediately lowered the fed funds rate to the lower boundary (i.e., close to zero) and vouched to leave it there for as long as necessary.

On top of that, the Fed restarted the quantitative easing program, buying bonds to lower the yields on the short and long end of the curve. Furthermore, it opened USD swap lines with other central banks in the advanced world to provide liquidity and advert the strong dollar theme.

It worked.

The dollar initially appreciated as the world looked for safety in the face of the pandemic, but then the Fed’s plan entered into effect. Slowly at first, more aggressively after, the dollar started to lose ground across the dashboard.

Everything appreciated in dollar terms – the euro, the Australian dollar, the British pound, equities, and commodities alike. The bearish trend on the dollar was so strong that all investment houses forecasted an even lower dollar in 2021.

They were right.

The so-called reflation trade, where U.S. equities advance, the dollar declines, and risk-on dominates, was the theme for most of the first quarter of the year. However, the dollar started to show some strength recently on the back of a faster economic recovery, impressive vaccination campaign, and a U.S. administration that delivers.

What’s Next for the U.S. Dollar?

As we head into the second quarter of the year, the dollar trades with a mixed tone. On the one hand, it gained against the euro since the year started.

At the start of January, the EURUSD pair traded above 1.23, and last Friday closed below 1.18. Because the euro has the biggest weight in the dollar index, the move lower in the EURUSD exchange rate led to a reversal in the DXY.

Gold made a new all-time high in 2020 – it traded above $2,000 last summer but is in retreat ever since. It is barely holding above $1,700 at the moment, and fears of higher inflation in the United States and the developed world are not enough to fuel a rally in the yellow metal.

The problem for the reflation trade and gold comes from the fixed-income market. The U.S. yields are rising, and whenever this happened in the past, gold weakened.

Put it simply, rising yields mean that investors flee the safety of bonds in search of higher returns in riskier assets. Effectively, it means that confidence is back and, thus, gold suffers as investors do not look for protection anymore.

Higher yields also bode well for the dollar. Hence, before betting on a lower dollar, investors should first monitor the fixed-income market and interpret where the yields will go.

All in all, the second quarter will be extremely interesting. If the yields continue to rise, the dollar will have a hard time weakening.

FXOpen Blog